A conventional loan is a safe, transparent loan that follows the rules put in place by Freddie Mac and Fannie Mae. Typically over the long haul, a borrower will save more money on a conventional loan over an FHA loan.

Conventional fixed rate loans are the gold standard in lending and have been for the past 30 years. They are an ideal product for anyone who wants to save money, and still know they’re getting a fair deal.

If you can make it happen, conventional loans offer several appealing benefits to qualified borrowers:

1. Offers transparency and peace of mind

A loan that conforms to Freddie Mac and Fannie Mae’s guidelines is a loan that follows the rules.

Since implementation of the Dodd-Frank act, things like negative amortization, balloon payments and prepayment penalties have become illegal on fannie and freddie loans. It’s safe to say on a conventional loan you’ll know you aren’t being taken for a ride.

.jpg?width=600&name=Untitled%20Design%20(42).jpg)

Alternative loans still exist and are actually making a bit of a comeback; they are far less regulated, and don’t follow the guidelines put in place to keep both lenders and borrowers safe and thriving in our economy. Portfolio loans, Alt-A and Non-QM are all terms used to describe non Fannie Mae and Freddie Mac loans that may or may not have risky features.

This is not to say that some alternative loan programs aren’t great. Some are, but the fine print is small for a reason, and if you’re not an experienced borrower, and positive your best interest is being looked after by a mortgage professional you trust, conventional loans are the much safer bet for most people.

2. Stability in an unstable world

A conventional loan with a fixed rate gives you peace of mind in an unpredictable world. You will know exactly how much your interest rate and subsequent payment will be, regardless of what the market does over time, and what the current interest rates might inflate to.

Some folks like to say “the only constant in the housing market is a FIXED-RATE.”

3. Rewards good credit with lower interest rates

Conventional loans come with competitive interest rates, that tend to reward higher credit scores with lower rates. This is a good reason to research your credit score and credit history before you decide it’s time to buy.

If you have a low-end credit score, you’ll have time to repair it, and improve your score, potentially save a grip of money over time with the reward of a better interest rate on your loan.

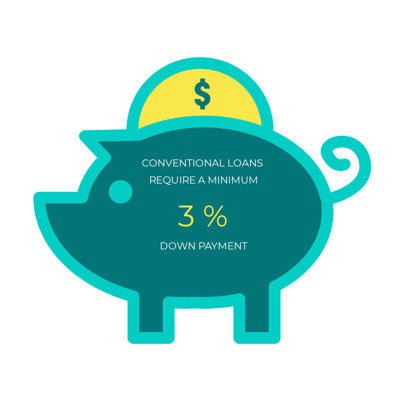

4. Low down payment options

You can put as little as 3% down to purchase your home with a conventional loan. It does require mortgage insurance if you choose this route, which increases the cost, but unlike a government loan, such as an FHA, the mortgage insurance does not need to last for the life of the loan.

Once you have enough equity in your home to reach the 80% LTV (loan-to-value ratio) threshold (of your original purchase price or appraised value), your mortgage insurance goes away.

5. Save money with a shorter term loan

Borrowers who want to pay off their home quickly and save money on interest payments can opt for a shorter term 15 or 20 year loan. Some lenders even offer as low as 10 year terms and intervals like 17, 22, 25 and 27 year terms to pay back a conventional mortgage. Making larger payments on a short-term loan, if feasible, can save tens of thousands, if not hundreds of thousands of dollars for borrowers.

6. Can be used for many types of homes

Conventional loans can be used for a variety of purchase types, including second homes, vacation homes, rental properties, multi-unit dwellings, and more. The rules for VA, USDA, and FHA approved property types vary from program to program, but the primary commonality is the fact that it MUST be used as a primary residence.

7. Often preferred by sellers

Conventional loans tend to be more appealing to a seller, especially in a crowded market where they have their pick of offers, and can help you get an edge over the competition.

Government loans that have a lot of paperwork and requirements can fall through, and take longer, which can cost sellers money. Most of the time things are smooth, but too many people will have heard the worst of the worst stories about FHA or VA appraisals going awry, and those stories, whether true or untrue, can cause a seller to accept a conventional offer over a government offer.

8. Tend to be cheaper to close

All government loans have a funding fee included in the loan amount (although VA funding fees can be waived with service related disabilities). Because these up-front fees are financed into your loan they are easily overlooked, but in truth they are a substantial cost that you do pay on each and every month.

Conventional loans avoid these up front fees, which makes them more economical. Conventional appraisals are typically about 10-15% cheaper than government appraisal fees as well. Although it isn’t always the case, most of the time conventional loans will be slightly cheaper than their government counterparts.

Just to be clear, we’re not bagging on other types of loans. There are great loans that are truly the better choice in certain circumstances. But as a broad generalization, those who qualify will usually benefit from a conventional loan, and build equity more easily by saving money on the cost of purchasing their home.

.png)